You may find yourself in the situation where there’s a shortfall. You may not have enough regular or guaranteed money coming in, to pay everything you need.

Whilst at first glace, it’s quite alarming, again we speak from experience, it’s not always as negative as you would think.

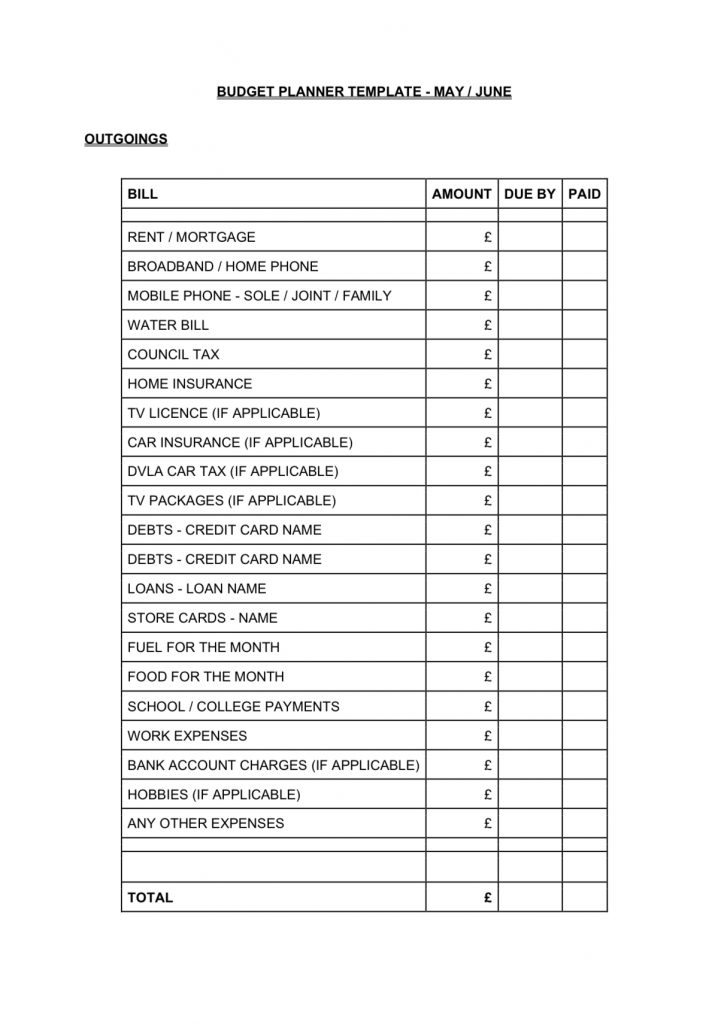

You have the tools to go through every detail of your income and expenses. This should help you discover areas where you can reduce your outgoings or increase your income.

For example, if you pay for a gym membership you may have to cancel it or put it on hold. Are there any bills which you can reduce (we obviously can help with reducing your utilities or earning an extra income).

Calling the companies and being honest about your circumstances can help. Any debt company will want to go through your income and expenses so this is where your budget planner will be handy again. I’ll be doing a whole blog on this next week.

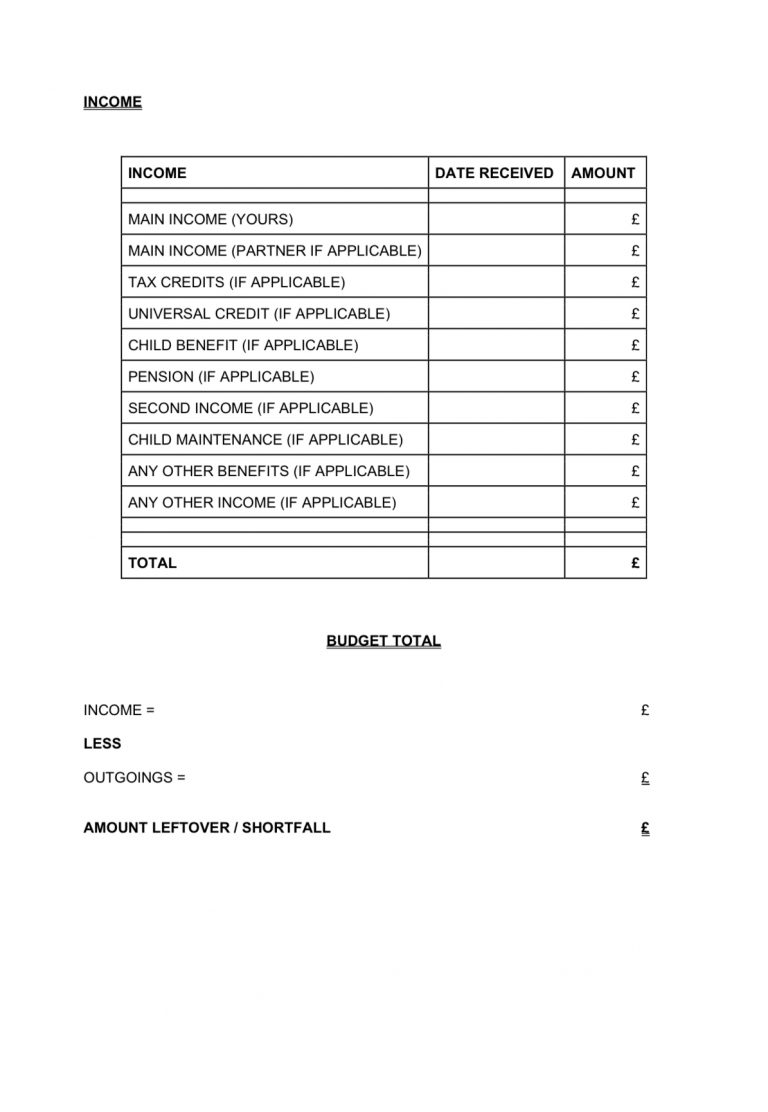

You may choose to bring more money into your home with overtime, taking on a second job or work from home opportunity. Selling unwanted items on Facebook Market, Vinted, carboots, eBay etc can bring in extra cash. A busy carboot on a nice day can be very worthwhile sometimes. One man’s junk is often another man’s treasure.